Claim: YouTuber Keshav Bedi claimed that Oil Bonds and Bank Recapitalisation Bonds are similar in nature because they create a repayment burden for future governments.

Our examination found the claim to be MISLEADING.

How We Examined the Claim:

We examined the details of Oil Bonds (Reference 1) and Bank Recapitalisation Bonds (Reference 2) as published by official government sources.

Oil Bonds were issued to OMC’s (Oil Marketing Companies) to compensate them for oil subsidy losses. These bonds had the net effect of deferring subsidy payments to future governments. For example, oil subsidy was given in the year 2007 but taxpayers would be paying for it in 2022.

Bank Recapitalisation Bonds were issued from the year 2017 onwards to add more capital to PSBs. (Public Sector Banks). Typically, these bonds were bought by a bank and the same money was used to buy more share capital in the same bank by the government. This shored up bank balance sheets through internal restructuring with government support. On the government’s side, against the bond liability created by these bonds, the government created an asset of additional share holding in these banks. This balance sheet strengthening exercise was done to meet international risk management best practices, namely Basel III. Basel III standards afford a higher level of safety to the depositors and to the overall banking system which is the backbone of our economy.

Conclusion:

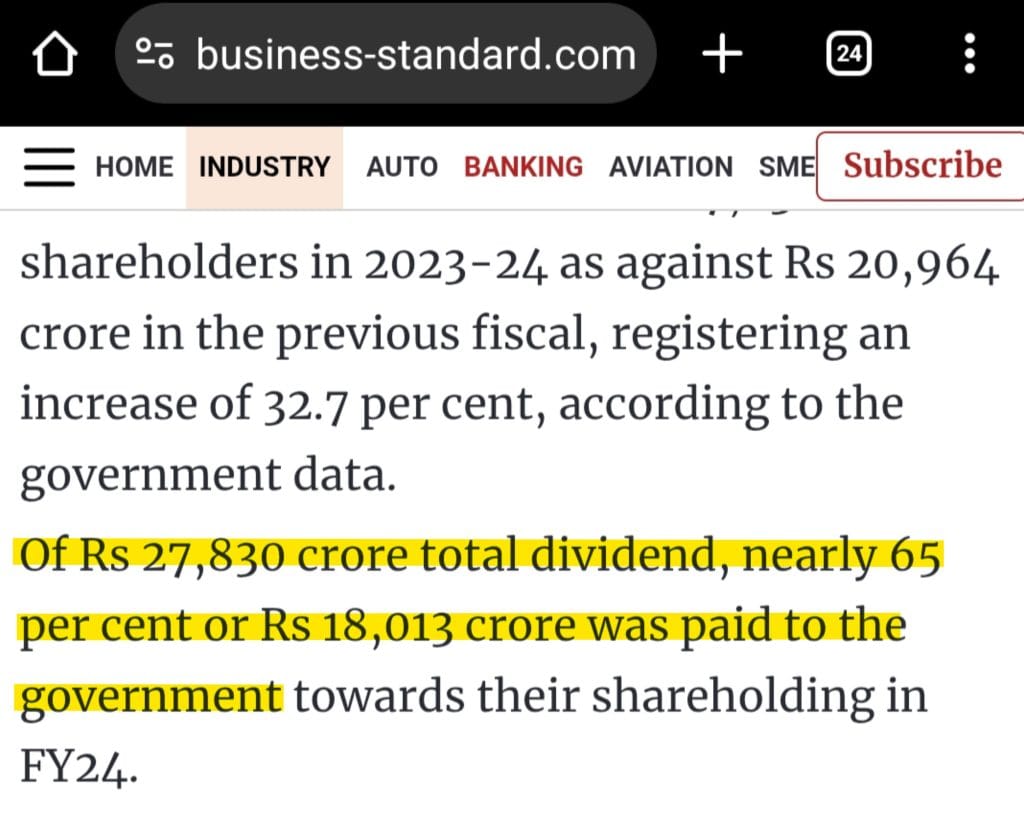

The argument that Bank Recapitalisation Bonds will create a liability for future governments same as Oil Bonds is a weak one because all borrowing creates future liabilities. Such an argument also seeks to mischaracterise the criticism levelled against Oil Bonds. The critics of Oil Bonds criticized them because they were not issued to create investments or infrastructure but to defer an expense to future taxpayers. Oil Bonds created a misleading picture of India’s financial health while creating additional expenses for future governments. They did not fund creation of assets or infrastructure. Bank Recapitalisation Bonds on the other hand, were issued to strengthen banking system and depositor protection by complying with international best practices. These bonds created an investment of higher shareholding in banks against the liabilities created by the bonds. These bonds are funded by the same banks that benefited from them. Investment into PSBs also earns dividend income to the government, with PSBs paying Rs 18,013 crores dividend to the government in 2024 (Picture 1). Comparing a bond issued to fund investments with a bond issued to defer expenses is highly disingenuous. The following simplified example will make the difference clear.

Borrowing to buy a house (Bank Recapitalisation Bonds):

- Creates an asset that typically appreciates in value

- Provides ongoing benefits (shelter, potential rental income)

- The debt is backed by a tangible, valuable asset

- Generally considered “good debt” in personal finance

Borrowing to visit a fancy restaurant (Oil Bonds):

- Pays for consumption that provides no lasting value

- Creates debt with no corresponding asset

- The money is spent and gone, but the debt remains

- Generally considered poor financial practice

Therefore, the claim is Misleading.

References:

- pib.gov.in- Ministry of Petroleum & Natural Gas, ‘Oil Bonds for Recovering Losses of Omcs’, release date: 27th April 2010

- Press Information Bureau, Press Release by Ministry of Finance, ‘Recapitalisation of Public Sector Banks‘, release date: 5th January 2018

- Business Standard article titled “Public Sector banks’ dividend rises 33% to Rs 27,830 crore in FY24”